|

|||||

|

|||||

|

|

|

|||||

|

|||||

|

|

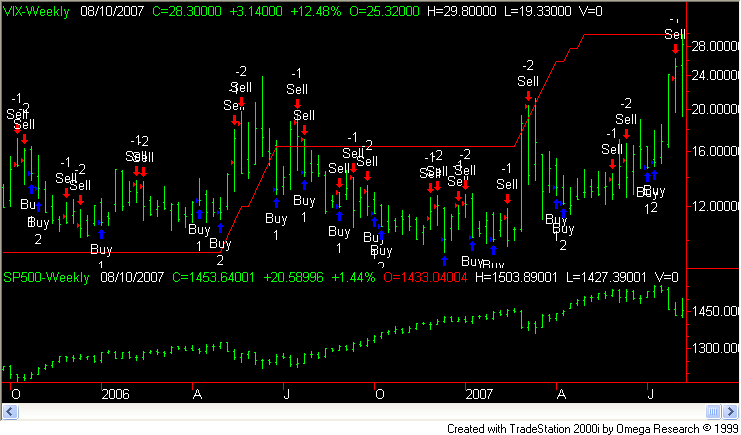

VIX TRADING / Volatility Directional Trading System / Low market Correlation trader /

Feb 10/07 - Volatility waited till week's end to show that investors have become too complacent but was it just to shake out the so called weak hands as the economy hums along at a steady clip? We at marketpit have our own measure of volatility and it is important to us in our own trading for one very important reason. When volatility is rising (signaled by an up arrow) there has been a net market gain of 7 spy -the S&P 500 ETF- points since 1992 (when the SPY started trading) and a net gain of 25 spy points when a second signal of rising volatility is added (these are gains on short positions). What does this mean to risk? This means that by being out of the market while volatility was rising we could have gained the entire upside potential of the S&P 500 by only being invested while volatility is declining (shown with a down arrow). Our risk is lowered by almost 50% while maintaining the full potential of the upside. What this does not mean? Is that we would have caught every rally and avoided all declines ( that would be impossible and do not believe otherwise). But over the time period covered 1992-2007 by being out of the markets while volatility rose we could have been safely invested in t-bills and made an extra few percentage on our capital.