Weekly Commentary

"Prices move until the marginal efficiency of other assets falls in line

with the rate of interest" Keynes 1936 |

Aug 11/07 - It is the white knight to the rescue of the

markets in the form of the Fed and the ECB. It was a volatile week but the

markets ended virtually unchanged. Why did the Fed feel the need to

intervene since we have not had a healthy correction in over 3 years? The

main reason may have been that banks do not want to lend to other banks in the

form of overnight deposits because they may wake up to another bust company.

After all, why does your bank have so much leverage? One of the reasons is

that this may be has do in fact to do with the low volatility that we have had.

This makes the return on some assets much lower and may also reduce the risk but

you have to get leverage. The other important point this week has been for

corporations that borrow from commercial paper sales. This week the CP

rate jumped to 5.5% which is up 0.32% for the week. This is important

because if they are now having a harder time getting short term funds it will be

that much more difficult for consumers. Look for credit card rates to move

higher in the near future and our estimate for commercial paper is rates of

6.5%. The widening of credit rates does not bode well for the

economy into next year as capital now has a higher hurdle to produce good

returns. Finally, our studies of commodities have signalled a top in the

CRB index and the market may have called Bernake's bluff of not saving the

market. Look for the potential of a rally on the Bernake PUT.

July 21/07 - The week was going good until GOOG came out with

earnings that were great but the market was looking for reasons for a sell-off.

However, we feel that this is a temporary shift in market behavior as even

string earnings are temporarily now considered not to be enough to push stocks

and markets higher. Let think of it like this - if google has great

potential and has great earnings then my stocks that have just average earnings

are not likely to perform. This seems a bit flawed in our opinion and we

expect the market to bottom sometime mid week as volatility is likely to spike

over 19 as measured by the VIX. In the bond markets there was a flight to

quality even as subprime hit new ABX lows and the Alt A mortgages also began to

decline. This decline in the

Alt A mortgages

is disturbing and any signs of further weakness should be regarded as coming

higher default rates from the re-setting of mortgage rates as the teasers begin

to come to maturity. The USD continued to make new lows as more bad news

about the presidents ratings fell to record lows but if the dollar is so low

then why is everyone buying the treasuries - including foreigners (perhaps there

is no where else to move all that liquidity). That liquidity is what we

expect to move back into equities.

July 14/07 - The best comparisons in investing may not come

from the world of psychology as has been the recent revival of behavioral

economics. In games of psychology the end is often know and games are played

in attempts to get the maximum payoff. Total profits can only be increased at

the expense of the competitors and the brokers take a guaranteed slice of the

pie as "we" compete against "them". In comparison to biology the end of a life

cycle can only be estimated and there is not some attempt at a one time maximum

payoff but a steady stream of food for conversion into energy. Nutritional

intake is of up most importance as starvation can lead to stress and eventual

death, often as short as a few hours for bats and a few weeks for people. So

why do people play the markets based on theories of the Prisoners Dilemma, Game

Theory, Home Run Hitting or random behavior like coin tossing? Coin tossing may

not be all that random as its outcome is impacted by the force the coin is

tossed, wind speed and in some cases cheaters may be at work fixing the system

by extracting a fee for each toss. A need for a steady income stream is the

promise in hedge fund as there profits are from alpha as opposed to beta which

tends to be too volatile. The markets may have an upward drift but an aging

population does not have time. Our SPX/USD trading model held long through the

biggest one day rally in over four years but volatility is suggesting that the

rally is limited and next week earnings release promises more variance in

stocks. In the bond markets our systems point to higher rates as 10 year rates

are coming off lows of 5% and short term corporate rates are starting to move

higher.

July 8/07 - Interest rates dropped briefly below 5% on the 10

year notes but then reversed course and made a run to 5.20% and short term rates

also moved higher. The sub prime fiasco continued with rumors that BS hedge

funds were being offered 10 cents on the dollar for their subprime bonds. This

is hard to believe and if the fund would have been forced to liquidate then

there would have been a firesale. Anyways the truth is that the market has

already built sub prime issues into the market prices and that if further

adjustments are needed , well at this time we do not know. Next week will bring

earnings reports from Alcoa and Pepsi and a host of smaller companies and we

expect volatility to pick up in anticipation of the week after when Intel and

Yahoo among others report. As Yahoo recently replaced the CEO we can expect

some surprises on the downside there perhaps. Short term upside on the SP seems

limited at this time. With rates rising and the China market having slipped 15%

from its high it appears that our commodity call last week may have some time

to run on the downside.

June 30/07 - It was a volatile week but volatility and

interest rates fell by the end of the week. to that tune we will no longer be

providing signals on the SP or the nasdaq and have discontinued our COT service.

It is of our opinion that COT is delayed and that upon analysis there is margin

value being added by delayed data. On the equity front we can get much

better information from variables such as interest rates, inflation, and market

volatility. For it is these factors that lead us to the equity market in

search of better returns. There was an interesting development this week

as our CRB index is flashing a sell signal for

Monday. The CRB index has been moving sideways for a number of months but

the one wildcard will be oil. On the interest rate world short term and

long term rates continue to signal higher rates over the coming month. In

particular this may be lead by higher commercial paper rates as investors start

to move into other investments.

June 24/07 - It was a volatile week and the bond market was

the place of the flight to quality. Most of the news was about the sale of

bonds at Bear Stearns and now Merrill was wanting to sell off some of its hedge

fund bonds as sale prices but at the last minute Bear came up with collateral

for the fund. In the markets there was little news but investors jumped

back into bonds for now. We continue to look for a higher yield curve and higher

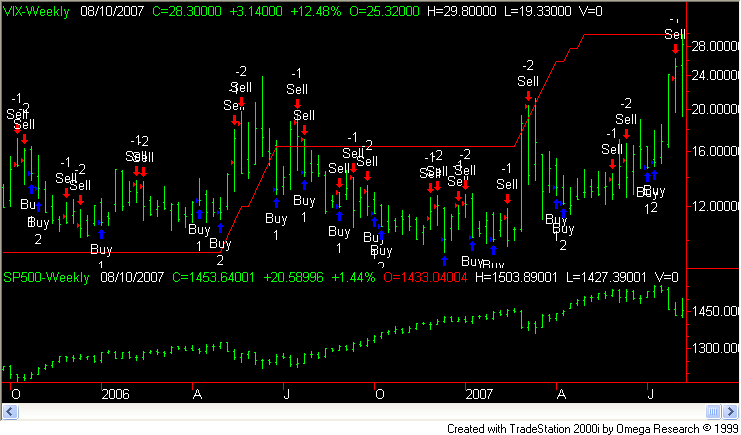

rates. Please click on the graphs on the right for more insight into our

model predictions.

June 16/07 - Are projection of higher markets came to bear

fruit after a down early week and the bond market delivered higher rates.

By week end it was clear that the core rates are falling on the inflation front

but the inflation rate including food and energy is on the rise and fast.

Will this filter into the core rates? That is the million dollar question

as the Fed's do not want to pay further benefits and the biggest core of

inflation is the Owners Equivalent Rent. The biggest jump we noticed in

commodities was the jump in the

prices of wheat (read as bread and dough for donuts amongst other items).

We believe the yield curve

will continue its upward move and rates will be higher in the coming months

unless there are changes in the flow money and inflation expectations.

June 9/07 - The bond market does not answer to equity

holders, it only needs to be compared to other countries. The bond market took

a beating this week as the 10 year bonds topped the magical 5% mark with a

jump. The 10 year bonds last topped on June

28/06 at 5.24% and began heading south. Bonds need to be compared to rates in

other countries as money is liquid and currency fluctuations can be hedged.

Further, the demand for money from the big takeovers is up 50% over last year as

the smart money has been issuing the junk bonds as fast as they can. The yield

spreads have been incredibly low considering that deficits are climbing, and as

we see from the Canadian and European

Markets higher rates are not just a US issue. A strange occurrence happened

this week as all three of our daily directional timing systems issued a strong

sell signal. Further, the SP-USD strategy gave a sell mid week and the markets

turning strongly lower Thursday. In the coming weeks there will continue to be

pressure on US bonds and the yield curve will move into higher positive

territory as investors remain anxious about parking there funds into either

equities or bonds. The Group of Eight summit also this week may not be going

all that well as Russia had some tough words prior to the meeting and this may

have changed the agenda and sentiment of attending members. In the coming week

we expect further equity market upside and decreased market volatility. There

may be unwinding of the carry trade as the Japanese Yen

is projected to move higher. On the 30 year

bonds an important point will be at 107.00 on the futures market.

June 02/07 - The week set new highs in the

S&P and bonds made a run to the 5% mark.

The missing piece of the puzzle is the projected rate of

inflation. Our models are looking at a jump in inflation over the

coming weeks. The other inflation (hedge) GOLD

is also going on a buy on Monday. Retuning to the main story of bonds

this week we expect rates to move higher leading to lower bond future prices

(this includes the bond ETF TLT). The

yield curve is moving higher and short term rates remain low relative to

upcoming inflation expectations. Amazingly, our earnings

expectations system is pointing to higher earnings and some of this is most

likely due to corporate buybacks (such as IBM).

May 26/07 - The markets continue to flirt with record highs

but for some reason are unable to penetrate into new highs and remain there.

In particular the small caps have been hit hard after making new highs on the

Russell2000. The equity markets may experience a small sell-off early in

the week to make a recovery over the next few weeks as our volatility strategy

is jumping in with both feet early Tuesday morning. There is however a

different picture over on the bond markets as the recent sell-off has left a few

bond traders scratching their heads as the economic indicators have been

conflicting over the last few weeks. Finally, the REIT market seems to

moving lower in sympathy with bonds and we are working on a strategy for this

volatile market.

May 19/07 - Wall Street was abuzz with takeover rumors as

Microsoft finally made a play to buy out aQuantive Inc. for about $6 billion in

cash. Will this be the bet it makes to offset the technological advantages that

google currently has? The equity markets fell then rose and ended where they

basically started the week. The story was different for the bond markets as the

10-year rates moved from 4.68% to 4.80% and bonds trended lower. Our

expectation has been for both short term and long term rates (next critical move

of 5 year rates above 4.7%) to move higher with a

flat yield curve in the near future. Rates have stubbornly stayed low with

world liquidity looking for places to park their excess funds, this week however

China made a 3 billion investment with Blackstone in a sign that they are

looking for higher yields and have tolerance for more risk (but 3 billion is not

a sign of a significant change of policy). Alan Greenspan joined the Bond King

of Pimco, as pimco was right last year on the housing market but incorrect on

the path of interest rates. Gold finally made its move lower and our systems

have been on the wrong side for some time with this commodity but correct with

anticipation of a higher Canadian Dollar (another commodity play). Finally,

there was a paper released by ANDREW W. LO of Massachusetts Institute of

Technology (MIT) -

Sloan School

of Management on Where do Alphas Come From?: A New Measure of the Value of

Active Investment Management. Among other items it discusses the returns of

funds based on "measures the portion of the manager's expected return due to

static investments in the underlying securities, …the forecast power implicit in

the manager's dynamic investment choices".

May 12/07- Interest in VIX Futures set a new record this week

as some investors got the jitters on Thursday. This brings us to an important

observation about market sentiment. Investor sentiment is often identified as

being at extremes at major market tops or bottoms. However, market sentiment

is being pushed as a market-timing tool, even with the following problems.

Often data is collected from individuals over the previous week and thus it is

already delayed, other investors have access to this data before the user

(people seem to forget about this lag), sentiment is most often a past

reflection of the markets and not a harbinger of things to come and lastly

sentiment is an observation of feelings and not where one is putting their

money. With the above issues, then one can conclude it would be useless in any

trading models and that is why web pages that display this data (and often

charge for it) do not show it in any useful trading model. The eyes have a way

of deceiving us on relationships / correlation's. In the bond market prices

moved lower as an increase in UK rates put pressure on this side of the ocean.

We expect to see continued weakness in bonds and a rise in VIX in the coming

week.

May 06/07 - The markets have been up for five weeks in a row

and the odds of a six are on the low side. There has been much talk of

market momentum but according to a new paper from

Hwang, Soosung and Rubesam, Alexandre,

"The

Disappearance of Momentum" (March 2007) it has all but disappeared since

2000 from the markets. If this is true then mutual funds and those that

depend on momentum based strategies will continue to under-perform the market

for the foreseeable future. Market volatility will

spike higher this week as we enter a critical zone in volatility over the next

few weeks. The bond market is on a sell on our daily system as the lower

USD has yet to have a significant impact on other markets. We would go as far to

say that the dollar does not matter as all the players have their eyes on the

markets.

April 28/07 - Leveraged buyouts may be great for the stock

world but for some bondholders (such as BCE) they are experiencing downside

pain. Why would a takeover not be so good for all? One possible reason is that

when the company is taken over and stock is retired (bought out) the new private

company will issue new debt to finance the company and to some extent the

buy-out. This may hurt current bondholders as the company margin may cause

rating agencies to cut debt from investment grade to junk levels. In this case

current bond holders are in ambiguity as they are uncertain if there bonds will

also be retired along with the stock. Investors in the bonds react

asymmetrically to such ambiguous news. In this case the current bond holders

have some information indicating the arrival of bad news. This is intangible

information, yet the market has decided to act upon it as it was tangible

information. Future buyers of the bond (the people who set the price when

ambiguity is high) require compensation for the increased uncertainty.

Ambiguity differs from volatility as volatility is about market expectations and

ambiguity is about the quality of the information. When investors begin to cast

doubt on tangible information then the result is volatility. Our

strategies continue to support a market rally but

volatility will be making a comeback over the next two weeks unless new

information leads us to believe otherwise.

April 21/07 - There seems to be a lot of pessimism out is the

markets these days and the Margin Debt levels may not be a good reflection of

real margin as the short sellers are part of the borrowing. Previously short

selling was not this big but with true hedge funds this has changed and we must

re-evaluate some common markets indicators in this light. I will also add that

when any data is delivered with a lag that it losses much of its punch as others

have access to the data prior to the public. When traders start to look for

market correlation's they are bound to see that B follows A and that it happens

more often than not. This off-course is just a quick computation and is often

only tested on the last data period available (as this the most recent in

memory). I would caution that as follows B more and more that the scenario is

more likely coming to an end, as other traders will have also picked up on the

pattern. The pattern is definite to end when someone publishes a paper of a

book on it, just like the incredible January Effect, presidential cycle or the

Dogs of the Dow. In this end we will be changing our ES trading model to one

that has been a more consistent winner and uses variable different than the

current version. The following week appears to remain bullish with the

exception of volatility and lower earnings from the not so high profile stocks

in the SP500. If there is a market drop coming it will not be a buying

opportunity as have been the past drops which were accompanied by

earnings estimate increases such as 1987,2003 and

even the recent 416 point plunge for the Dow Jones Industrials on Feb 27/2007 on

our earnings model.

April 14/07 - Market Earnings

are the lifeblood of the markets, if there was never any possibility of profits

nobody in their sane state of mind would invest in stocks. Thankfully, the

earnings of the S&P 500 are positive and lately have been positive in a big way.

As go earnings so normally goes the market and earning estimates are the

biggest big business in the investment industry. Why then are earnings

difficult to predict even with good knowledge of a company or industry?

Earnings Projections are just as difficult to forecast

as the markets due to the number of variables in the

economy. For stock valuation, company specific earnings

are in many cases he basis of buying the stock. This is

apparent on earnings day, as any deviations from the

forecast are meet with extreme volatility. Earnings

forecast keep broker analyst busy writing reports for

current and potential clients, this helps to sell as the

firm appears to be providing investors something

tangible of value that the client would not have the

time to research. It may produce a tangible report but

the variables used in the report are far from being

tangible to forecast - it is not like measuring how high

a tree will grow using measurements such as soil

condition, moisture and hours of sunshine among other

factors that can be directly measured.

The truth be told as the economy changes so do the

fortunes of any individual company on average. This

means that earnings rise and fall along with the

variables that impact the economy and the costs of doing

business. Some of those costs are the cost of

borrowing (such as outstanding debt that most companies

have) and the ability to price products based on costs.

This means that as these factors change so must earnings

estimates. Normally estimates are revised when earnings

are released as investors have an appetite for the

unknown.

Our

model of SP500 Earnings Forecast is based on macro

indicators mentioned above and on various estimates of

potential risks (volatility of earnings). As in the

Black Scholes model of option pricing we believe that

the best estimates are made with the most current

information. At this point we do not attempt to focus

on individual companies but the market as a whole. The

free cash flow model is the preferred method of

corporate evaluation but that is more difficult to

calculate (with fewer errors) so the earnings estimate

may be the next best thing. Further earnings come out

quarterly and give investors something to bite into

until the next quarter.

April 08/07- The market has

been reduced by some to just a mathematical formula full of ratios and models.

This may work for them in the current environment but unless they show the

willingness to adopt then those models will in the future expire. What has been

neglected is the human will to change to new and unexpected events or to carry

markets to an extreme. These can not be measured with accuracy but we can

attempt to time when these changes may happen by looking at volatility. In the

markets, volatility is the temperature of the markets - the higher the

temperature the more extreme the markets tend to be. At periods of high

temperatures are the times of opportunity as market participants are open to new

ideas as older held beliefs may have lead them astray and filled their thoughts

with uncertainty. This is also the point that collective behavior works its

magic, the magic of leading the crowd in the right direction. This is similar

to a group of people guessing the number of jellybeans in a container even when

individual guesses are very incorrect. On the markets, interest rates may be at

the point of high influence as investors have been placing bets on bonds at a

higher rate (as witnessed by increasing futures volumes). Rates now look poised

to move higher. Vix is also signaling more surprises in the coming

earnings season.

March 31/07 -The markets are

the home of uncertainty and of bears and bulls attempting to figure out the

future course of the markets. This uncertainty is all in the data according to

the Fed and it will be resolved by the data, so if the Fed is unaware of the

state of the economy how could other investors be too sure. Well, nobody can be

certain no matter how good our observations but we need to have the ability to

out think our opponents in the markets. This may be called gaming or a version

of the predator/prey model but in the markets the net sum is zero minus

commissions (some may argue that there is an upward drift in the markets that we

have not accounted). In gaming the market, the biggest mistakes are often the

times that the market is moving fast and we are unable to cope with this sudden

volatility. There does not exist any single market model or formula that

describes possible market outcomes. The best we can accomplish is to identify

the possible variables and give a probability of possible outcome. Any possible

theory we hold about the market has value in explanation, not of the future

outcomes. The most important factor in trading may be flexibility, to take

corrective action to avoid serious risk. Market theory needs to take into

account that people react, learn and anticipate other traders behavior. Market

uncertainty is not going to be solved by an abstract formula, as information

itself is imperfect. Finally, even if a pattern/formula were effective in

determining the market direction, the markets nature would assure that the

future pattern would be altered.

March 24/07 - The market got a heart jumpstart after the Fed

meeting and the shorts were scrambling to cover. As the subprime market

starts to stabilize and some hedge funds think they are getting a deal by buying

these loans at 96 cents on the dollar. Well, we think this will come back

to haunt some of these early vultures. This brings us to the leveraged bet

that individuals and funds are taking these days. The low volatility

periods have been the best of days but making overleveraged bets are a sure path

to ruin. This is the equivalent of writing naked puts and getting a great

sharpe ratio until some future point. In the risk business this is called

left tail risk or negative skew. Why are we discussing leverage at this

time? Just think back to a few months ago when customer margin

accounts were at record highs. Well that seems to have also blown away but

there now exists the potential that consequences from that event may hit the

market. It is consequences of consequences that moves the markets and not

the latest number of the macro economy.

March 17/07 - It was the week of options expiry and some

believe that markets tend to decline in such week, but we have not been able to

test this theory. What we do know is that options expiry can not be as

important as before as now we have option expiry every week on some options and

month end expiry on many others. I would not suggest trading options (due to the

time decay factor and the timing and directional factors) but it plays an

important role in traders beliefs. In for one, informs us of the implied

volatility for stocks and indexes and this has historically been very accurate

in predicting the variance of markets. If this were not the case then we

could arbitrage the opportunity to our benefit. Alan Greenspan continues

to warn of a slowdown in part to profit margins being at record highs and we are

monitoring this closely, as employment and capital spending goes in the

direction of profits. In the bond world, interest rates continue to dance

around in the 5% region for short term rates and the longer rates do not feel

any impact from the subprime fiasco. The S&P based on USD

returns remains bullish as does volatility.

March 10/07 - The markets moved higher and the subprime

mortgage market has tanked along with the ABX index as some of the liquidity is

drying up. Can the subprime damage be limited to holders or will it spread to

other mortgage providers? One stock that will be impacted in the coming weeks

is Fannie Mae (FNM). We suspect that most private equity and hedge funds have

hedged themselves and that one need to closely follow the REIT market (^RMZ on

http://finance.yahoo.com) to notice any cracks in this large market. We

have been working with a number of models over the last few months and the SP

measured in USD funds appears to show good gains and has been benefiting form

the "YEN carry" trade confusion. The confusion surrounds how big this market

is? It has been our experience not to measure markets where there is no index

for comparison but to stay informed on how investors may be affected by such

news. Market volatility topped off early Monday morning and has been heading

south rather quickly as volatility sellers (option writers) have taken this

opportunity to sell options to anxious bears. It appears that many traders were

hoping for a 10% correction (that much talked about number) before moving back

into the markets but the market is least accommodating when investors have a set

target. This created a large pool of investors that were sidelined and have

been coming back into the market over the week with the realization that the

markets are moving against them. Next week we expect a top early Monday with the

markets heading lower for the remainder of the week. In the bond markets a

strong jobs report on Friday confirmed that the economy is still strong and that

earnings are growing at an inflationary pace. Bonds at this point are also on a

sell but Gold stocks (XAU) are signalling a rally ahead.

Finally, we will continue to closely monitor corporate earnings as the earning

margin may be at unsustainable levels and future corporate profits may be lower

than anticipated.

Mar 03/07 - It starts in the east and spreads to the west

that about sums up what we saw this week on Wall Street. Our quantitative

models remained locked in buy mode. It is our belief that some of our models

use similar inputs as those used by hedge funds thus they are subject to jumps

in volatility. A few weeks back (Feb 10) we advised being out of the market

while the VIX models were signaling a rise in volatility.

This saved us a lot of headaches as we prefer to only play the long side while

volatility is falling and diversify into plays on GOLD

and the Bond Market. Someone must have

hit the panic button with investors as this was a total surprise for all

involved but the ABX index might have provided some insight into credit

problems. There was not much news but the selling seemed to come out of nowhere

but appeared everywhere, with the exception of long term bonds. The selling is

in fact playing upon the moral factors that produce panic and investors try to

stay ahead of the selling on the other side of the world. In the end it will

depend on corporate profits but if a trillion dollars is wiped of the market in

a week then buying power drop somewhere in the economy. On a final note, the

selling in Gold may simply be a result of traders not selling losing positions

and taking funds out of the gold market to cover margin calls and our Asset

Allocation Model is recommending buying bonds and shorting the Russell2000 as

equity premium is too high for these small caps.

Feb 25/07 - Surging worldwide liquidity has been accompanied

by rising bond and equity markets. The equity markets have been helped by

an ever rising corporate profits, as a percentage of GNP they are at 40 year

highs. this level has not been seen since 1965-1966 and the low was

reached in 1982, the beginning of this great bull market. Corporations are

a mixed group that finds funding where it is cheapest ie. either by stock

issuance or bonds and today they have expansion plans on their mind (private

equity), they can get cheap financing from the bond markets. this is

evident in the junk bond market where the spread over treasury is razor thin.

Why has the default rate remained so low? It is nearly impossible to

default in the markets continue to purchase your new batch of bonds or they can

be repachaged to appeal to investors. An example of this is the housing

market, people have had access to easy money - think subprime. The

subprime market is now having its own problems (see the implode o meter site at

www.ml-implode.com ) or you can look up

the ABX index, which has dropped like a rock. The funds are beginning to

draw up so I suspect it will be a tough year for that market. This brings

to mind the GM fiasco earlier this year as their debt was cut to junk but the

stock continued upward soon after. The difference that comes to mind is

one is a corporation vs individual and liquidity was there for the taking vs

todays liquidity. In the bond market short term rates rates are moving

higher (slightly) and longer term rates remain in a downtrend. The equity

markets look poised to move higher and Microsoft that we mentioned a few weeks

ago as a short looks to have bottomed out with a 63% of moving higher over the

next weeks. Any sign of trouble continues to be in the low VIX readings

but with all the bearishness out there it is difficult to not remain bullish.

Feb 17/07 - The world of asset allocation has a major impact

on equity markets as funds flow into markets that are expected to benefit from a

robust economy. As all assets are in competition with each other, money has a

tendency to be allocated to those who are able to best invest it in growing

sectors of the economy. This may not always be the case but in capital markets

this is the general logic. Our interest at Marketpit.com is to allocate funds

between the 10 year treasury and the S&P equity market. This is important as

investors will have to decide to be conservative by buying bonds or to be

expecting strong earnings from firms in the S&P. A stock could be considered a

bond in perpetuity with an uncertain rate of return but the bond has a constant

stream of income. The price of uncertainty is called the risk premium as

investors do not want to hold stocks when they decline. Our strategy is to use

the Stock vs Bonds analogy. It is a comparison of the Russell 2000 divided by

the 10 year treasury and tells us the ratio of of the cost of debt vs equity

risk. With a current ratio of 7.5 you could buy 7.5 units of bonds or 1 unit of

the small cap index. It has moved between 3.5 and 7.8 since 1993. It made a

high in early 2000 and is just now approaching the same level. What this means

is that you could have invested in Bonds and have made the same return as the

Russell 2000 over the last 7 years with much less volatility and a lot better

sleep at night. However based on our analysis you would have been invested in

equities since 2006 and have made double digit gains as compared to bonds over

the last year. In the bond markets the yiel curve surprised us and is heading

south with short term rates poised to head higher. Gold and the XAU gold

stocks remain on a sell and we may see some of that sell-off this week. On

the equity markets we are bullish on the SPY and the QQQQ with both strategies

on a buy. One caveat is that volatility remains at low levels and our

volatility strategy is calling for an increase.

Feb 10/07 - Volatility waited till week's end to show that

investors have become too complacent but was it just to shake out the so called

weak hands as the economy hums along at a steady clip? We at marketpit have our

own measure of volatility and it is important to us in our own trading for one

very important reason. When volatility is rising

(signaled by an up arrow) there has been a net market gain of 7 spy -the S&P

500 ETF- points since 1992 (when the SPY started trading) and a net gain of 25

spy points when a second signal of rising volatility is added (these are

gains on short positions). What does this mean to risk? This means that by

being out of the market while volatility was rising we could have gained the

entire upside potential of the S&P 500 by only being invested while volatility

is declining (shown with a down arrow). Our risk is lowered by almost 50% while

maintaining the full potential of the upside. What this does not mean?

Is that we would have caught every rally and avoided all declines ( that would

be impossible and do not believe otherwise). But over the time period covered

1992-2007 by being out of the markets while volatility rose we could have been

safely invested in t-bills and made an extra few percentage on our capital.

Feb 04/07 - Trading is not about being right on your opinion,

it is about getting is less wrong on your trading than the competition.

The market place is a place of price discovery mixed with a large amount of

noise and people seem to presume there is such a thing as smart money and that

somewhere there are individuals who know what is the right time to invest long

or short. The being right should be replaced with being less wrong and we

will make some great strides towards better trading (and less stress). We

all bring a unique perspective to the market, some are technical, trend

following, fundamental, quantitative, momentum, risk adverse volatility traders

etc.... and somehow prices get accurately reflected for the most part.

This week in the equity markets should mark a down week as both the emini and

qqqq strategy are on a sell signal. There is also evidence that Microsoft will

experience weakness as Vista sales may not go as expected and thus earnings

revisions may be needed. In the bond markets are short term trading is long but

over the course of the month we expect to see higher rates along with a positive

yield curve over the next few months. One of the big events will be a fed

refunding this week and there is a possibility that it may not be as strong as

in the past. Market volatility is near all time lows and we continue to

expect a jump in these numbers this week.

Jan 27/07 - It has been a challenge for us to develop high

frequency trading models and we have spent countless hours with tick data and to

date there has not been any major market anomalies that are tradeable (that we

can find). One approach would be to move away from a quantitative approach

to a more qualitative approach. This strategy would be moving away from

structure to an unstructured approach, move from a counting based system to an

observation (interview) system, act like an insider as opposed to a part time

player, move from the PC data figures and into the market (ie the market may

have language), and instead of having pre-defined data in advance just

work out the numbers as one goes along the trading day. Further, the

cause-effect would move from looking for causes to one in which causes and

effects could not be distinguished. Finally, you would need a measure of

risk aversion and a time limit for your trades. At this point these are just

rough idea's but if we put effort into them, they could be the basis of highly

profitable strategy. In the equity markets there was a small pullback that

the SP system was able to capture and volatility will continue to rise in the

coming weeks. The bond market displayed more weakness as there was a large

number of issues hitting the market at the same time. Gold remains strong

but the XAU (gold index) remains on a sell and the 650.00 point on gold markets

a temporary top. If are strategies both turn up this week look for a

strong rally to follow.

Jan 21/07 - There are a number of issues with fixed trading

systems, non greater than the human desire to override them and the quest to

optimize. Readers of our site will have noticed two systems - one for the

QQQQ and the other for the SP500. Often they are in contradiction of one

another and the investor needs to chose which one will give the better signal

(choice). It has been our experience to only trade the signals when they

are both pointing in the same direction. If we add in the weekly

volatility then more confusion arises as volatility only has a 65% correlation

with the markets but most of the bull market moves (85%) has occurred in periods

of declining volatility. This week oil remained under pressure and this

has negatively impacted the Canadian Dollar, as Canada's major export is OIL.

The gold market remained in a small uptrend but the XAU remains bullish and we

suspect that the price of gold having topped recently will limit any move in the

XAU. Our equity strategy is to remain bullish and we are attempting to

reconcile differences when more trading systems are used (ie 5 separate

strategies). Readers advice welcome.

Jan 13/07 - It was a great week for the markets as all equity

markets ended much higher. As the 5 day January barometer ended and some

people picked up stocks cheap. Markets are not thinking in terms of

diversification, they are looking for gains from alternate investments.

Some of the emerging markets had problems as Chavez nationalized and the India

and China markets fell back from record highs. Interestingly, these

markets also are large user of Oil that coincidentally had a fall of its own.

Whether this is a correlation or causation remains to be seen. Market

volatility remains at low levels but may get some help in April with the SEC

approving changes over at the CBOE that will allow trades to become

leveraged with the help of options. It will certainly get the options

market heated and drive some volatility into the markets. This is

important because it will change investor trading behavior and we feel some

trading systems will stop working and others will improve in performance.

Trading continues to be all about leverage, if it is offered then traders will

use it esp. with the current environment of low volatility. We expect

volatility has bottomed for now. As the year

starts it appears that interest rates are set to rise for durations over 5 years

and the narrowing of the yield curve continues. Gold has an excellent run

up on Friday of 13.00 dollars and we remain bullish on XAU stocks of which we

prefer Goldcorp(GG) and Iamgold (IAG). We remain surprised as our CRB

strategy has not given a sell signal and our Oil sell came late this time.

Our equity strategies are off to a great start with both the SPX and Nasdaq

long.

Jan 07/07 - Lets start the year on the right foot and look at

what matters in investing RISK - the four letter word that most money managers

would rather not talk about because they think there clients are not

sophisticated enough to understand. The forms that risk comes in all lead to

the fact that in some way it was unexpected. You will hear managers of hedge

funds cover themselves by saying something like " there are storm clouds

gathering on the horizon" but that does not add value except when what you are

really hedging is your opinion. We have access to data other investors use and

we make some of the same expectations as it is important to understand what

others are considering. Over the years our models have proven that they are

able to anticipate changes in volatility and thus have us prepare a defensive

position or establish short positions for more aggressive traders. Risk is akin

to a drivers blind spot, you do not worry about what you do not notice until it

hits you. That is the importance of doing your own research. In the equity

markets traders were changing positions as conflicting information about future

fed moves came in the form of lower employment numbers from ADP and then the

opposite came from the Labor Department on Friday. Job growth is important but

not as important as corporate profits, as no profits then no new hiring. The

Bond Market reacted by ending the week virtually unchanged - it is still making

up its mind even as Bill Gross from Pimco thinks there is room for a full

percentage point off the current level. Over at out Bond Trading Site

www.cmetrader.com commercial paper is

actually signaling higher corporate rates We prefer to let the market act

and we make up our mind along the way from vital changes that are near tem.

Gold sold off for a number of reasons over the past few weeks but at this time

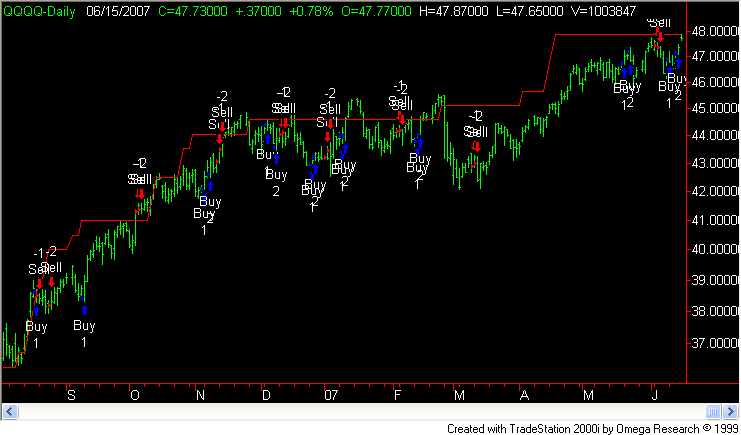

the XAU (Gold Stocks Index) in again on a buy. Click on chart name to the

right for clear viewable charts showing long and short entry positions.

Dec 31/06 - We will not be making any significant market

projections for 2007 as the next 24 hours are difficult to forecast with

reasonable accuracy. However, I will comment that there are two types of

risk in the market - those that are close and those that are in the distant.

If you let your mind wander you will be able to come up with a number of outside

risks, such as the political changes coming to the US Senate, the situation in

Iraq, the value of the US dollar as the world standard, Middle East problems,

etc.... The problem is some of them may evolve to become real problems and

some will just linger the way they have for the last number of years. What

you can not do is base an asset mix on this type of logic. But there are

investors you bet on such outcomes and we can attempt to game them over the

longer period. One type of investor who likes worst possible outcomes are

Gold investors. They buy the metal not as a hedge but as a bet on chaos.

In the short term is where you may attempt to squeeze this type of player as the

metal can fall faster than it rises. In the equity markets near term volatility

remains low but we have sell signals on both the QQQQ and SPX. The 10 year

bond rates are headed higher and the yield curve may soon become flat from

negative. If the earnings announcements are not positive then expect that

earnings have topped out. If this happens we will display our earnings

chart that topped out in early 2000, just as the sharp Nasdaq drop started. Best

wishes to our readers for the new year.

Dec 24/06 - This is a time of reflection and pondering plans

for the future. On needs to tune out the TV and decide what is important

to them and to view the future in an optimistic view as any other view will

freeze out any plans we are making. Life has a way of moving forward, the

move can often be described as random but purpose full for a better life forward

for those who embrace the future. All our equity strategies are on buy

signals for the week ahead. This last week looks like those who wanted to

relieve themselves of the pressure of holding into the new year (bears) sold

into the hands of those with a optimistic outlook. Looking forward to

Santa Claus and a rally by the bulls. Best wishes to you and your

family this holiday season.

Dec 18/06 - In the markets momentum is a force that has been

recognized for some time and that came to investors attention in

Momentum Strategies LKC Chan, N Jegadeesh,

J Lakonishok - The Journal of Finance, 1996. People are in search of some

simple rules to explain market reactions and often times there comes along a

theory to do just that. The above in part was a function of the

environment of the time and the time period over which the study was conducted.

Factors not recognized were trading costs were much higher and people committed

to positions for longer periods and market liquidity was not as we have today.

Even today there are samples of market momentum in small cap securities but the

liquidity factor makes it unavailable to larger traders to take advantage of.

We have read hundreds of papers on the markets and the more we read the more

holes we see in such strategies and the one's that seem to be a market anomaly

quickly disappear as traders take advantage of it. just remember if you

notice a market anomaly to not publish it ( now you know that it gets published

because it most likely is not usable). In Newton's world as in the world

of momentum trading a body in motion stays in motion unless interfered by an

external force or by friction. In the market there is no need for external

force as the markets are able to internally generate their own volatility.

The market volatility has been at rest recently, next week we expect this

condition to reverse as the equity markets may start to head lower. Why

they may head lower is the yield curve is now heading higher and OIL prices are

signaling higher prices. In the bond markets a move in the 10 year yield

above 4.63 will signal lower bond prices. In the gold market the metal has

been on a sell for the last few weeks but the XAU is signaling higher gold stock

prices in the coming weeks. Finally, I think they rally we had recently came

ahead of time in place of the Santa Claus week rally.

Dec 10/06 - Asset diversification is not the hot topic it

once was as the words alpha and beta are now the in words in money management.

I t would appear that assets these days are moving more in synch than the days

of the day traders in the 1990's. In this regard the latest casualty is

hedge funds as there returns as well as even small cap securities move along

side the performance of the SP500. What this means to traders is that

diversification is not giving investors the desired results of lower broader

risk. This of course means that is does not matter what asset group you

own as they will all move as a group. To the doomsayers it means that when

markets drop there will be no place to hide, not even in alpha selling hedge

funds. The doomsayers are just too prevalent in the gold markets these

days and that was why we advised selling gold last week. Further, we

expect market volatility to remain low and even a possible rebound in the Us

dollar in the coming weeks. The qqqq market remains in a long position with the

SP500 in a sell causing us to wonder if the market may be going nowhere fast.

This week we will also be introducing a daily bond trading strategy based on the

returns of the 30 year bond as our readers have been requesting more bond

analysis (based on search engine results coming into

www.cmetrader.com our bond site).

Dec 02/06 -

Asset

Allocation is the major determinate of returns for mutual funds. How

much of the return is attributable to this strategy 40-100%? In a quote

from the paper by Ibbotson and Kaplan "We found

that, on average, about 90 percent of the variability of returns of a typical

fund across time is explained by asset allocation policy". This is one of

the reasons why when markets drop funds need to purchase bonds but it is also a

reason why when stocks rise funds buys bonds. In the first scenario funds

buy bonds to avoid further market volatility and in the second scenario bonds

are purchased to keep an 60/40 allocation of assets. There is no inverse

relationship

between stocks and bonds but there is a strong case for a rolling

relationship or the theory of the Fed model. In either case the above is

partial evidence of herd/flocking behaviors in the markets (the behavior only

helps to explain the market reactions - not the triggers or combinations that

start them). This brings us to month end and the above should help explain

why market participants are in a flurry to shape up their portfolios and often

invest access cash into stocks ( as 401K contributions roll in on a timely

basis) and funds show that your cash is not idle ie. your fund manager is

earning his pay. In the commodity markets Gold along with gold stocks are

now likely to head lower. In the equity markets

the S&P was lower by 0.30% and the QQQQ fell by almost 2%. The bond markets were

the stars as rates continue to fall.

Nov 26/06 - Company profits continue to propel the market

higher, as the number of potential problems continue to pile up. The

problems are numerous such as the takeover of Congress, the Iraq war and the

housing bubble to name a few. The real rates for the housing market have

us convinced that it no longer makes sense to continue to purchase housing

as going forward the volatility has increased. But the profits for corporations

has stabilized according to their stock price movements. In fact, our

volatility indicator is showing a sell on Monday (lower volatility ahead) even

as the bears are warning of low VIX reading as trouble ahead. The commodity

markets continue to show strength with the possible exception of OIL and Gold

(including gold stocks) are the best buys over the next few weeks. The

gold markets are helped by an up move in stocks and not by bear markets.

Further, market shorts may be establishing new short positions and that needs to

be reduced prior to any sharp market drops. In the equity markets the QQQQ

remains on a sell as the SPX (SPY) remains the better buy. For investors,

it may not be wise to take short positions due to the higher risks and as

markets have an upward bias over the longer terms. On the bond markets,

lower rates are cause for concern in the US dollar and bonds remain a buy on the

10 year bond on any rates below 4.65% .

Nov 18/06 - High frequency trading is the use by managers of

minute to minute data to find a statistical advantage over the competition.

Most of the competitors in this game are hedge funds and proprietary desks at

major brokerage firms. It is difficult to access the returns on such strategies

but it is fair to assume that because of the shortened time frame in use that

the trades are highly leveraged. Some of these firms may have discovered

anomalies that allow them to take advantage of their competitors weakness such

as limited capital, algorithm trading patterns unearthed, or simply luck.

In the field of high frequency trading, random walk is at home as can be

expected so why do these firms exert such effort and time to find a tradable

system/strategy. We would suggest that each firm by itself is too small to

account for major moves in the market, but if most firms behave in a similar

fashion then there may be some underlying strategy that may prove profitable.

One of the ideas that has been of interest to us lately is how traders view risk

and the time allowed in trades. As the risk has a limit as does time then

traders risk is a moving target that gets bigger as time moves forward. It

is when the time horizons overlap that opportunity may become available -

traders all act in concert. This is best displayed by the recent rally as

trading times collided with bigger risk (lower volatility). Anticipating

the reactions between groups of traders offers the best opportunity to profit

that we are aware of. In the markets the QQQQ strategy is short and gold

continues to hold in rally mode. As short term rates do not drop the yield

curve is widening as longer term inflation

expectations remain contained. On a final note, our

cot data/charts are showing high levels of small trader bullishness, even as

large traders are reducing positions.

Nov 12/06 - It has not been out intent to be a rehash of the

weeks news, but investors seem to be looking for pages that somehow make sense

of the markets by using the news. Does the news make the markets?

Well if that where the case then it would be the journalist that were the

wizards on wall street. No, sadly it is the news that follows the price

action of stocks. Companies are part of the accomplice in the news story also.

When there is good news to report then there is often a stock run up prior to

the official news ( the news that the company could not hold in and let all

their associates in on) but when the story is sad and not favorable then

all attempts are made at plugging any news leaks for as long as possible (in the

extreme case like Enron). Thus it is like currency traders running around

with news that China plans to diversify its US dollar holdings, this was right

after the election and seems more a political maneuver that policy change.

Come on, you never tell anyone what you are about to do before you do it in the

markets - otherwise the sharks would beat you to the punch. In the markets

there was a short term upmove that most likely has run its course as the QQQQ is

flashing a sell for Monday morning. In the bond markets

short term rates are on course to head higher but

the longer term is less uncertain (currently signaling lower rates). The

Gold market has come back to life as well as the commodity game in general -

look for higher prices soon.

Nov 04/06 - Risk is not just a four letter word, it actually

has meaning in many languages but to big traders it means volatility and time.

Why is time important? Time is the difference between a profit and loss,

it separates the high frequency trader from the long term investor, it makes

options decay, causes future's traders to roll over contracts and it makes

investors nervous when time has not been good to them, there is only so much

time to decide when the margin calls come, and finally as the saying goes "time

is money". We could not have said that better ourselves and how true is

that statement. Most profitable traders have time frames for trades to

prove profitable, those that do not will have time decide their fate for

them. For long term investors time has the benefit of an upward drift in the

markets and a historically 6-8% premium over t-bills. Marketers use time

to mark how well they have done and in this case they chose the time from when

they bottomed. If you have investments you need to make time to review

them as needed, a trader daily and long term investors every few months or

longer. The time for a fed rate cut is gone, the time for higher rates is

emerging. the markets are signaling a sell along with increased

volatility. In time we will also change our stance, or time will force us

out of the game.

Oct 29/06 - The Sharpe ratio is a measure of excessive risk

per unit and risk in the markets is known as volatility. How do we compare

risk/price? These are two separate calculations/idea's and price is a

function of so-called value. Simply, price is what you pay and value is what it

is worth (according to some calculation). The best estimate of value is to know

the prices of a similar security (ie. look at other stocks in the same sector).

There are often a number of unobservable variables that make a difference in how

securities are priced (this is often a function of private information) but in

general the group moves as a whole. In an unknown future any two

securities that will profit equally from similar economic variables should have

similar current prices. The markets quants will attempt to model future economic

situations and thus there work is often centered not on price projection but the

future volatility/variance of a stock or groups of stocks. Thus the future path

of stock may be unknown but it may be possible to estimate a scenario of

possible future prices based on volatility. Thus if two stocks have a

similar future volatility then they should have a similar future prices.

In the markets we have been looking for volatility to rise over the last couple

of weeks. Short term the QQQQ and the SOXX index have least resistance on

the downside along with financial stocks. Financial stocks will take a hit

as short term rates move higher due to pressure on the US dollar. We

suspect that the election will have many court challenges as computerized

counting with no paper trail will leave open the validity of this technology

thus spreading the risk of unknown makeup of the future senate and US policies.

Oct 22/06 - When the average investor decides to buy or sell

a stock they will often be staring at the chart for longer than they would

otherwise. What are they thinking about? Is the chart somehow relaying

them information that they may have previously overlooked? Most likely

they just need some kind of confirmation that they are making the correct

decision and by looking over the chart they can conclude that they had spent the

time needed to make a good decision. Most of our readers will probably

notice that they are viewing the same information as before (a chart) and that a

chart has some value it does not display all the information about a stock.

Other variable to review may be insider trading, earnings potential, upcoming

market launches (new products), personnel changes, partnerships, recent

volatility, market strength etc.. the list is almost endless but we need to work

with information that we believe has value. This list will also change as

the market participation changes - it the 1990's it was the individual investor

who brought momentum back to the markets and after 2000 the hedge funds came

with their quantative methods. You need to have a strategy to deal

with the changing times and individuals. As Keynes said

"When the facts change, I change my mind. What do you

do, sir? The

markets this week were confused as the nasdaq declined and the S&P 500 posted a

small gain. Volatility came to new lows even as we have been expecting a jump in

volatility over the last week. In the bond markets any move to the upside

(greater than 0.05 ) by short term rates will signal a jump for t-bills up into

the 6% range. Inflation seems to have come under control and thus it would

appear that short or long rates have to logical reason to rise. Just as

when we are reviewing a chart, we are missing a lot of the picture.

Oct 15/06 - The valuing of a public company is difficult work

and often times even the CEO is unable to value their own company. When

analyst attempt the same they do no have access to the private info that the CEO

has, thus their estimates will likely fall where others that have come before

them have fallen. Our work is not to place a fundamental value on a company,

only if there are likely to show increased profits and if they company is

showing faith in itself by buying back its own stock. Over the last few

weeks many companies have done or announced both. The other part of an

investment strategy is the holding period one is willing to wait to see a profit

on your investments, a week is probably too short and forever is a long time to

wait. In the end it will depend on the investor and how long they have

been investing, new investors are likely to get nervous soon and the battle

hardy will have seen it all before. Another method of your time horizon may be

how one responds to market feedback - do you monitor your stocks inter-day,

daily or weekly. We are currently involved in working on a strategy that

trades about 6-10 times a year and is focused on stock selection, unlike the

charts that we have been posting on our site. The markets showed good strength

this week with the exception of a small plane hitting a building ( a small event

caused a large disruption in the markets) but they quickly recovered, plus some.

The important development this week was higher interest rates (esp the 10 year

rates), in the shorter term the 3 month commercial paper is close (if they move

10 basis point higher) to busting a new move higher.

Oct 9/06 - In the markets information and how one processes

that information are known as the information ratio. One has to be able to

produce high returns relative to the volatility of the strategy and this is

often why investors prefer a 60/40 stock-bond mix. Some have even suggested that

stocks are lower quality bonds with no repayment date. This may have been

the school of thought prior to the 1990's as the dividend and dividend ratio

played a major role in investment theories. Things change and we are

constantly on the lookout for small and major possible changes to the economy

and investor appetite. This week will likely mark the low end of the

volatility for the index markets ( with or without the North Korea test) as

window dressing season is over and the US political scene heats up. The QQQQ

looks to sell-off but the larger caps may continue to higher ground.

OCT 01/06 - The trader and the quant coming soon to a

brokerage house near you. It is expected that discount brokerage firms

will soon make available to retail clients trading strategies that were once the

domain of hedge funds. Will this be too much power in many hands or is

this a way to extend the life of failing strategies? What we do know is

that when in the late 1980's when technical indicators became standard on we

sites and easy to calculate on home PC's , that was the end of any remaining

value to technical analysis. The success of technical analysis was that is

was so easy a monkey could do it, one could argue that the quant systems now

becoming widely available will come complete with order placement. You

just need to select the system that works for you (this says little of the

system continuing to work). This may be a blessing to people who

understand how these systems function. TD ameritrade may start rolling out

this plan next month, Fidelity offers its WealthLab Pro Software, and

Interactive brokers offers advanced order placement strategies. For all these

brokers it will mean more trading and commissions in the long run ( people need

ideas to trade, even if they come from older hedge fund idea's). The

market this week displayed good upside and market volatility

continued to stay at low levels. The next week should be more of the

same as the QQQQ market should outperform the S&P

500. In the bond market bulls are running

the show with pessimists looking for a slowing economy.

Sept 24/06 - The Risk - as this week highlighted the Risk in

Model/Correlation trading and hedge funds that fail to diversify and what

happened at Amaranth. I will not go into the detail over at Amaranth but it is

fair to conclude that the risk was not contained. One of the core issues is that

risk advisers are aware of the type of risk their traders are engaging in. For

example they only hire risk managers who understand trading and global markets,

they can build, stress test and back test models, understand the trades placed

by their traders, are forward looking and keep an eye on these forward risks.

But how is it possible to keep a lookout on these forward risks if the forward

risks are uncertain. The risk manager will tell you they have their own risk

models (ie VAR) and understand the volatile nature of the markets. This is

essentially a catch 22 as the risk is known to most and those willing to accept

the risks will place the trades. Secondly, and much more important is that the

volatility often makes the price of an asset a highly unreliable function of

value. It appears the US dollar as a store of value may once again be in

question as lower rates prompt many to seek higher yields elsewhere and in other

currencies such as the Euro Dollar or

British Pound. Even as the equity markets ended lower

this week our models continue to forecast higher prices in the near term for

big cap stocks, the small cap stocks may be

moving in the other direction as witnessed by the

Russell2000 trading strategy. In

the bond markets the 10 year rates may be

dropping as some investors move out of housing related debt and into the secure

arms of federal debt.

Sept 17/06 - The markets are about business not politics, but

the politics of business interfere in the markets. This week oil prices

began a steady slide after the OPEC meeting last weekend and on reports of

Iran's willingness to possibly suspend any nuclear enrichment. However,

the bigger story not published was of states such as Saudi Arabia willing to

pump oil as needed and thus keeping inflation levels contained and not becoming

a factor in the coming congress elections. These are the types of items

that are difficult (impossible) to build into quant models. As per last we

continue to see lower "market volatility" and more market

surprises to the upside. As we approach

month end window dressing will pick up and corporate earnings continue to remain

strong. The Canadian markets are

dropping as as result of lower gold and oil prices but there was news this week

also of lower productivity levels. The

bond markets continue to show good strength as the inverted

yield curve looks to possibly start moving back to

a flat level in the coming month.

Sept 10/06 - The markets are composed of group's of

traders but they are not the sum of their parts. In studying behavioral

finance we have found it to place too much emphasis on how individuals act under

certain conditions. Most experiments are often carried out not in real

world conditions, but on university students who may act in an manner that is

expected of them. In the markets people carry out sentimental studies of

who is bearish and who is bullish and these studies at best are coincident

indicators. But people who are promoting such strategies will point to

such and such at time that the gains were strong or when you may have been out

of the market and missed a market decline. Market decisions are made based

on incomplete information ( much different than how we make other decisions) and

decisions are based on what others intend on doing (they are also awaiting your

decision). In the market, individual tendencies do not carry forward to group

behavior. In the commodity markets both oil and gold came under heavy selling

pressure as investors in those commodities gave up their middle east tension

premium. The market premium (as measured by the VIX)

is also due to drop in the coming weeks and thus the likelihood of

rising equity markets. The biggest

development this week would have to be a buy signal by the "yield

curve strategy". What this means to either short or long term rates

remains unknown at this time except that long term rates are closer to a bottom

than a top.

Sept 03/06 - The rational trader most likely does not exist,

among the general public that is, as institutions have implemented trading

strategies that remove the trader out of the equation. Trading rational is

difficult as we face pressures within ourselves that cause one to react to

market noise. Trading on fundamentals may be one of the better strategies

but investors know that prices often sway one way or another from the

fundamental value ( we are not sure how to value the markets in this manner as

even the future stream of company earnings is unknown past the next six months).

There has been much ado recently to inject physics into trading as particles

also behave in a random fashion but there are mathematical ways to measure their

movements and ranges. One of the drawbacks from this theory is that atoms

behave as atoms but people do not behave the same way in similar occasions.

People have till the last minute to make up their mind, and often that is when

they make a decision. All the talk of rational trader is often at a dead

end due to all the conflicting evidence and the high level of noise in

individual decision making. Our tendency is to focus on groups as there

will always be average behavior and we can expect traders to do as there

neighbors as birds do in a flock (ie flocking). Since not one trader

determines market direction the herd instincts are better studies for changes.

This week the markets had a good run-up in both

equity and

bond markets. The oil market came

down as the political premium dropped out of the price but we still see a rising

tend. The GOLD strategy continues to forecast higher metal and XAU

stock prices. Finally, the rational traders seem to have driven

volatility down to levels not seen for some time even as

the worst months to be invested comes upon us.

Aug 27/06 - It is the last week/new month and this is the

optimal time to be fully invested. This is due to a number of factors but

the biggest is mutual funds putting new money coming in into the markets and

some increased buying of the stocks they already own. The

yield curve may be signaling a coming slowdown but this often leads the

economy by about 3-5 quarters. The value of the yield curve is the expected

change in short term rates - as falling short term rates indicate slower real

GDP. Further, at the end of an economic expansion long rates often fall as

the decreased volatility in rates warrants a change in risk premium. This

is interesting a current market volatility remains below historical norms and is

signaling a lower volatility starting Monday until the

next signal. Along with this we have a bullish

S&P 500 index even as there is much reason to worry about the middle east

and rising protectionism. Do people feel the worst is over in the world

political scene, are people starting to feel confidence as the start of student

spending, are corporate earnings about to rise in general or are investors just

becoming too complacent?

Aug 19/06 - The market are a place for taking risks but we

often take bigger risks than we need to. Most people are often not even

aware of the type of risk that they are dealing with so let me begin with a

small list: equity risk, duration risk, yield curve risk, liquidity risk,

credit risk and volatility risk (to an extent even fraud such as has been

witnessed with Enron). If the market is about who has the best information then

we must define what type of information once is referring to and how does one

quantify the correlations. The customer is only concerned with the bottom

line, thus fund managers carefully monitor their volatility in relation to their

customer appetite for risk. Many customers may want risk but they will

move their funds when their account has been running a deficit in comparison to

the benchmark. Stock and bonds do have common features and it has often

been stated the distressed debt trades just as volatile as the common stock.

A few things to keep in mind when comparing the two: stocks have unlimited

upside, both may pay a yield ( dividend vs coupon), its just that stock do not

have a maturity date - thus often the overextended P/E ratio's. The Nasdaq

had its best week and volatility fell to a new recent low, the momentum of

small cap stocks remains strong. Finally,

the yield curve (often considered a

leading economic indicator) remains in negative territory. It has been

suggested that this is a harbinger of a recession and a downturn in the business

cycle. It is of our opinion that

short term rates will be

heading lower as the Fed is foreseeing slowing consumer consumption due to

the housing construction (read sales) slowdown that continues to suppress

lumber prices.

Aug 05/06 - It looks as the Fed will pause, we are issuing

our first sell signal on

commercial paper since our last buy in early 2004. It would appear that the

Fed is aware that the economy is weakening and does not want to tip the US into

a recession. The housing market is the talk of the economy as it has

driven both job growth and consumer spending. Most of the housing gains

can be traced to Real Interest

rates as calculated by yield on 3 month t-bills less the rate of inflation.

Since approx. 2002 until the start of this year the real rate has been negative

thus encouraging speculators to borrow funds and invest in real assets.

Assets were in effect rising faster than interest rates, thus the risk is

reduced for investors. However, as the rate is now positive (but below

historical standards) we are seeing a drastic slowdown is new home sales and

will likely see foreclosure notices also on the rise, as property values

increased the banks were willing to extend credit thus delaying any

foreclosures. However, if the Fed pauses here we will see inflation in the

form of a lower US dollar (higher import prices) and after an initial mini rally

in bonds an eventual sell-off. If the Fed does not act as expected we will

witness a sharp increase in investor fear (aka the VIX).

July 29/06 - If cash is King then mutual funds are holding a

lot of cash these days, but after the run up this week I suspect the cash levels

have dropped. Why hold cash and is it not a contrarian indicator?

Cash is normally held by open end funds to pay expenses and investor

redemptions. In time of high rates, such as today with T-bill rates in the

5% range it offers an alternative to the market. Some of these managers

may however be attempting to time the markets when in fact investors pay them to

select stocks, if they wanted to time investments they would buy a hedge fund.